Building Blocks

Distributed Ledger Technology

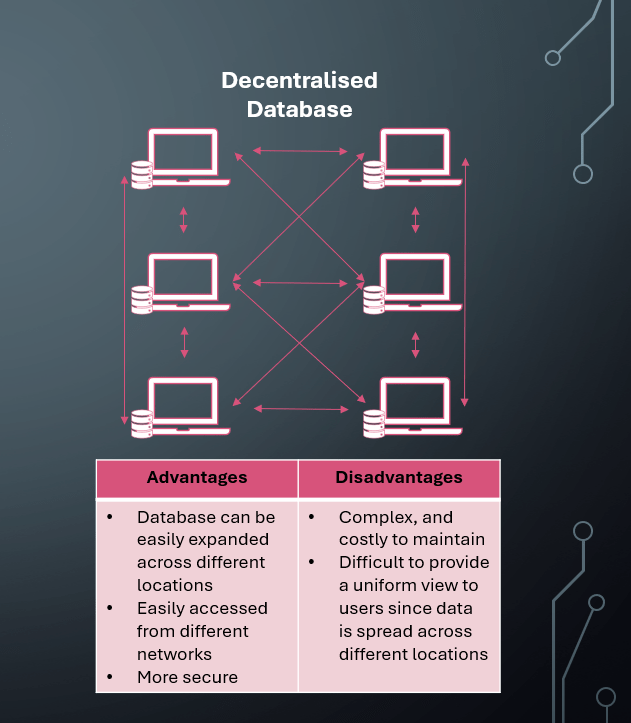

A distributed ledger is a system in which digital data is replicated, synchronised and spread geographically across many computers, sites, countries and/or institutions.

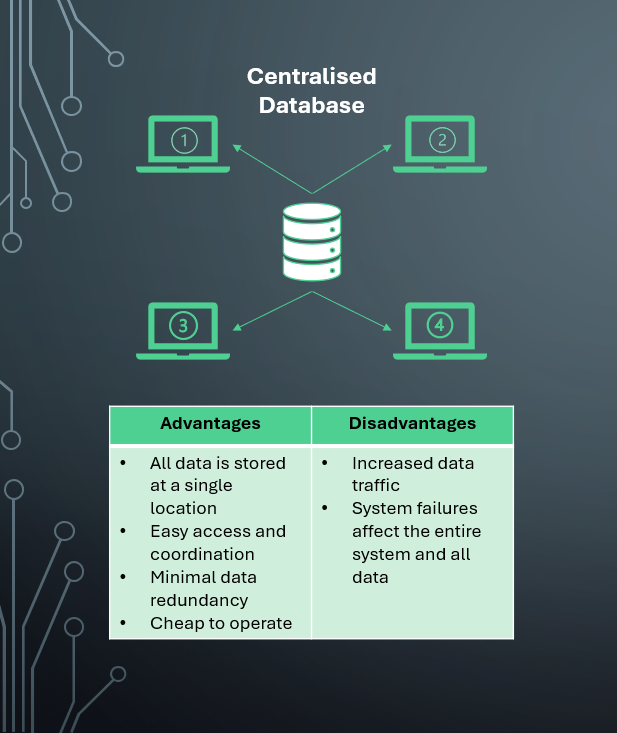

The system is decentralised, distributing administrative powers over a less concentrated area so there is no single point of failure. Instead, the infrastructure allows simultaneous access, validation and updates across the networked database. It differs from centralised infrastructure, in which decisions become concentrated with a particular group or entity.

The most common form of DLT is blockchain.

Blockchain

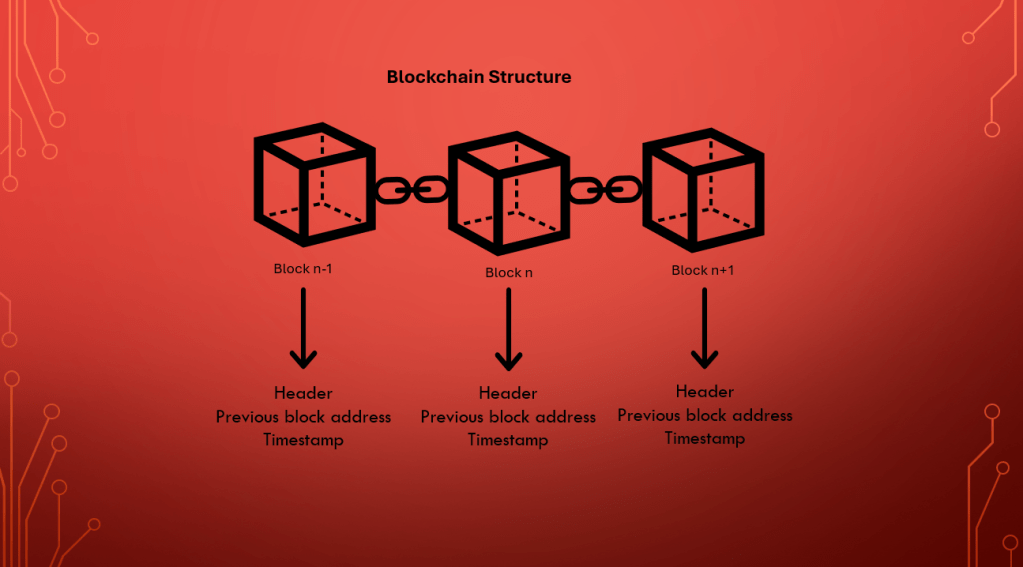

Blockchain is a shared, immutable and digital ledger that is distributed among many peers in a network. It records transactions and tracks assets as users trade.

Immutability ensures that a network only needs trust at the point of data entry. Once data is entered, accepted, bundled into a block and chained to the previous block, it cannot be altered without the whole network realising.

Each block contains timestamped data and is identifiable with a unique cryptographic hash containing that of the previous block.

The most well-known blockchain is the Bitcoin network.

Consensus

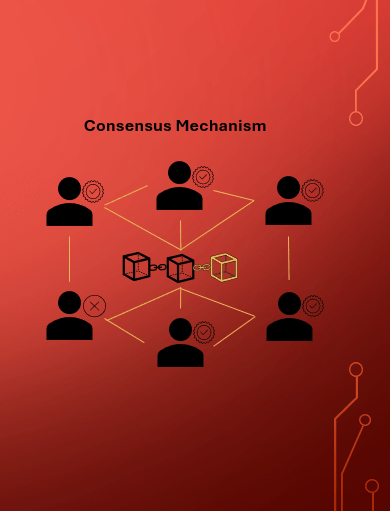

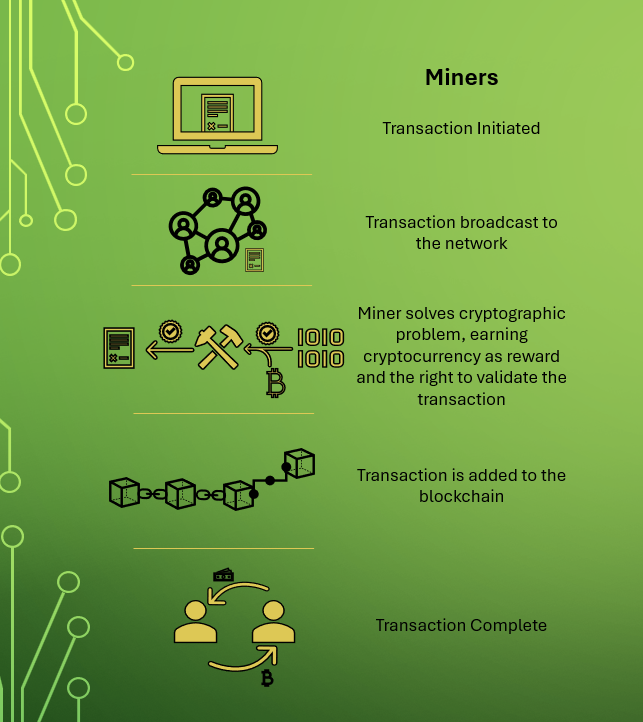

Blockchains validate data entry and distributes entries as records to the whole network. But the network must agree on the validity of records in the absence of a central authority.

It does this through consensus. Blockchains apply consensus mechanisms to achieve distributed agreement on the state of a dataset. There are various mechanisms, but all seek the same goal: efficient, transparent and secure agreement to replace centralised systems that suffer from inaccuracies or untrustworthy verifiers.

The leading strategies are:

- Proof of Stake – requires validators to hold and stake tokens for the privilege of confirming transactions and earning transaction fees.

- Proof of Work – requires miners to solve cryptographic puzzles to confirm blocks, earning rewards and fees for their efforts.

| Proof of Stake | Proof of Work |

|---|---|

| Block creators are called validators | Block creators are called miners |

| Participants holding network tokens can partake in validation | Participants need to buy equipment and energy to partake in mining |

| Security of the network is achieved through community consensus | Security of the network is achieved due to the upfront expense required |

| Validators receive transaction fees as rewards | Miners receive block rewards and network fees |

| Energy efficient | Energy inefficient |

Validation

Validators are crucial for confirming transactions in proof-of-stake consensus. They check whether proposed transactions conform to the network’s rules and ensure that a sender has adequate funds to complete the transaction. In most proof-of-stake systems, validators must deposit a sum of cryptocurrency as collateral in order to validate. This is known as staking.

A single validator is chosen at random to propose a new block. The proposer prepares the block and broadcasts it to the entire network. The community of validators verifies the proposal; only verified transactions are appended to the chain.

Validators are incentivised with payments of native cryptocurrency from the underlying blockchain.

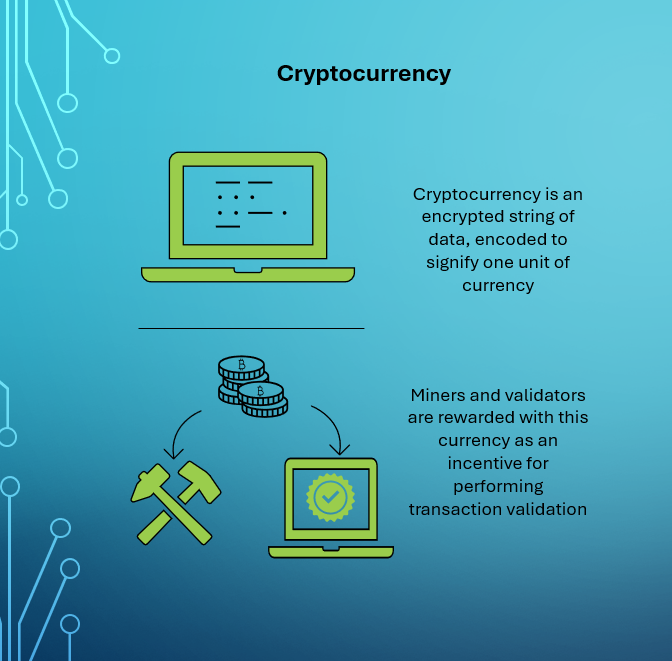

Cryptocurrency

Blockchains deploy native tokens so users can participate in network activity. These tokens – cryptocurrencies – are, therefore, digital mediums of exchange.

Blockchain stores asset ownership records on a digital ledger. Distribution of this ledger across many users increases network size, security and, in theory, attracts more users to partake in network economics. When users transact, they pay in the native token, like exchanging cash for items in a shop. In addition, users pay fees to validators for supporting their transactions in the form of native tokens.

Miners and validators receive native cryptocurrency for their work. New cryptocurrency is also minted from the network to continually incentivise participants to perform work. In a proof-of-stake model, validators stake their cryptocurrency as collateral to incentivise honest validation. In return, they get additional ownership of the cryptocurrency over time via fees, newly minted tokens and other reward mechanisms.

The first cryptocurrency was Bitcoin, released as open-source software in 2009.

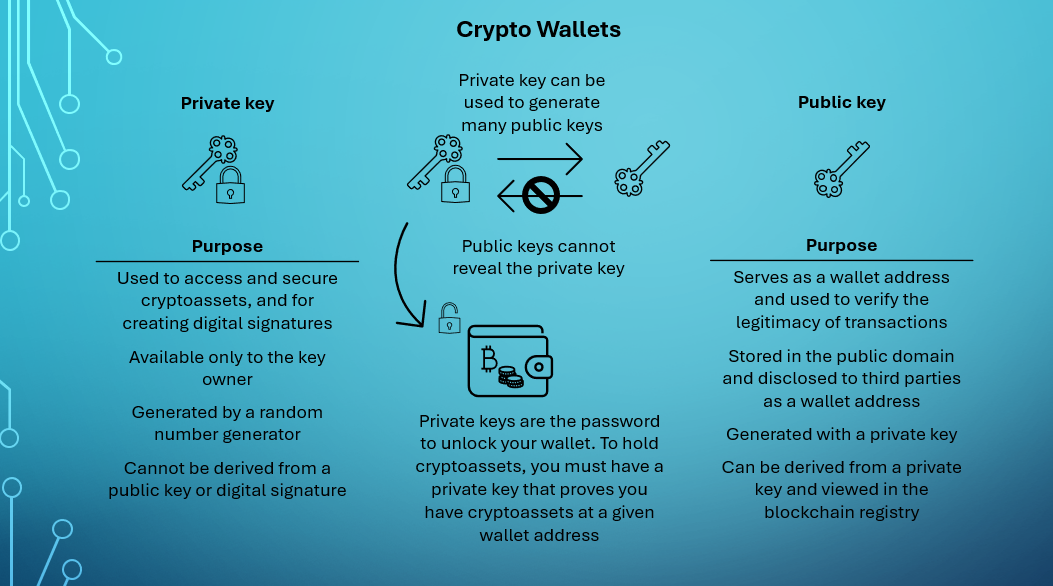

Wallets

Cryptocurrency wallets are software applications that access blockchains so one can use their tokens. Each wallet has a public address which identifies the specific wallet to the network. Cryptocurrencies are not technically stored anywhere; they are bits of data. The wallet finds all bits associated with a user’s public address and consolidates it in the wallet application.

Wallets support the send and receipt of cryptocurrencies. Typically, a user enters the recipient’s wallet address, chooses an amount to send, signs the transaction with their private key, agrees to support the transaction fee and sends it. More recently, wallets have integrated QR codes to increase efficiency. Receiving cryptocurrency simply requires the sender to enter the recipient’s wallet address. Once the receiver accepts payment, the transaction is final.

There are two main types of wallets. Custodial (online) wallets are hosted by a third party that stores one’s public and private keys. Coinbase is a prime example: they offer custodial wallets and hold customer accounts on the exchange. Noncustodial (offline) wallets require users to take responsibility for securing their own keys. This is most popular as it removes third parties but runs the risk that a user loses their keys (and, therefore, loses their cryptocurrency permanently).

There are two subcategories: hot and cold wallets. Hot wallets connect to the internet; cold wallets do not. Both are applicable to custodial and noncustodial wallet types.

Other concepts

- Miners – computer owners who contribute computing power and energy to solving cryptographic puzzles in a Proof-of-Work blockchain.

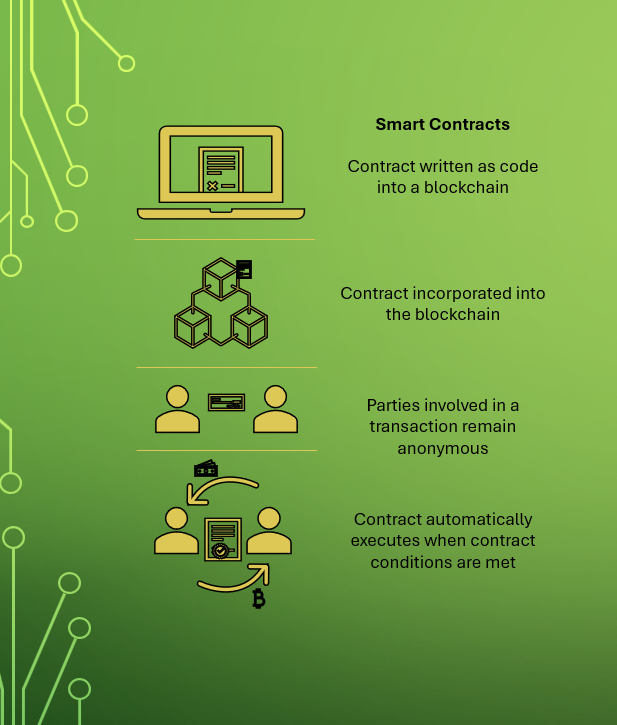

- Smart Contracts – a contract between two parties, programmed onto a blockchain, that automatically executes when a predefined outcome occurs (If X happens -> perform Y).

- For example, a smart contract for a sports bet: Person A bets Person B one bitcoin that England will win the Euros (Event X). If Event X happens, the contract executes and one bitcoin is transferred from Person B’s wallet to Person A’s wallet, without an intermediary facilitating the transaction.

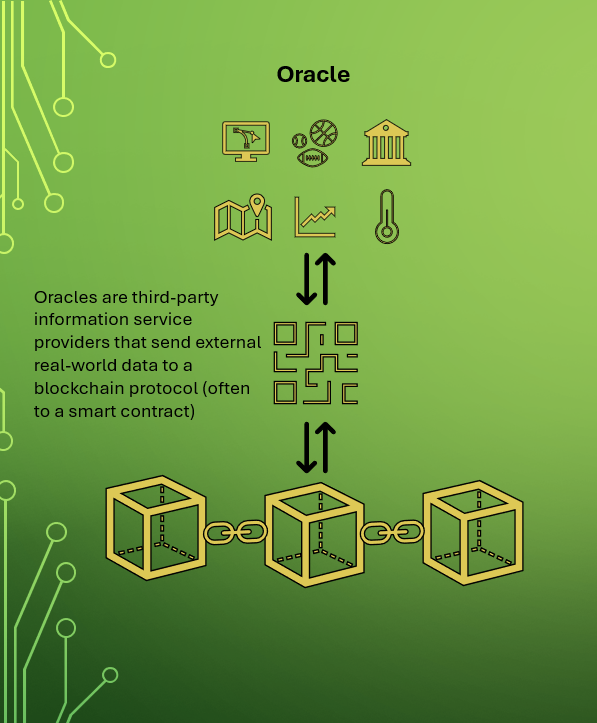

- Oracles – entities that connect blockchains to external systems, enabling smart contracts to execute based on real world inputs and outputs.

- With the example above, an oracle may live stream sports data directly onto the blockchain, so when full time is realised, the smart contract receives the information to execute.

- Tokenisation – the process of creating a digital representation of a real asset. The process issues a digital and unique representations of a real-world item so it can be used as an asset on a blockchain. Tokens can represent tangible assets, like real estate and art; financial assets, like equities and bonds; intangible assets, like intellectual property; or even identity and data.

What’s it all for?

Blockchain is praised as an innovation promising to revolutionise how entities interact and trade. Is this reputation warranted? Is blockchain needed?

Blockchain’s promise is heavily attributable to its ability to support trustless interactions. Two parties that do not know each other can exchange value without relying on an intermediary, unlocking new pathways for value transfer. This capability, made possible by protected and decentralised data storage, supports transparency and deters fraud or other malicious activity. It marks a change from traditionally centralised businesses which consolidate power to one entity. Other benefits of blockchain include:

- Enhanced security

- Blockchain creates an immutable record across a network of computers, encrypted end-to-end, rather than a single server.

- It is incredibly difficult for hackers to access or tamper with data, preventing fraud and protecting data against malicious activity.

- Personal data can be anonymised when transacting and access to it granted at an individual’s behest, increasing ownership over one’s data.

- Traceability

- Blockchain creates an audit trail documenting the origin and journey of an asset through every exchange, providing proof of an asset’s validity, production and usage.

- Data can be easily and directly shared with consumers.

- The audit trail can expose weaknesses in supply chains and identify tampered products, incentivising producers to act with integrity and improve product quality.

- Transparency

- Centralised organisations keep separate, singular databases: an inefficient method of storage that can expose customer data to hacks, attacks and manipulation.

- Distributed ledgers record and distribute data identically over multiple locations in the network.

- Transactions are immutably recorded with date and time stamps, so all participants can view the entire history.

- Any attempts to tamper with a record are observed by the whole network, greatly reducing fraud.

- Efficiency

- Traditional, centralised processes are often paper-based, time-consuming to validate, prone to human error and require third-party mediation.

- Streamlining processes with blockchain can help transactions complete faster, since there is no need for intermediaries.

- Users can store documents on a blockchain, eliminating the need for paper, and single, validated ledgers avoid the need for reconciliation.

- Automation

- Smart contracts automate transactions when pre-specified conditions are met, reducing human intervention to verify contract fulfilment.

- Automation increases efficiency of interactions between participants without compromising trust.